Recently, government decided to change the interest rate on savings instrument along with change in tenure with some of the National Savings Scheme. The change is effective from 1st December, 2011.PPF, NSC, KVP,POMIS and PO Deposits are savings instruments which are going to be affected from these changes.

For investors it is a mixed decision with some schemes becoming attractive for investment while some losing its sheen. Also the dynamics of interest rate will make things unpredictable unlike before where the end figures were well estimated during the start of investment.

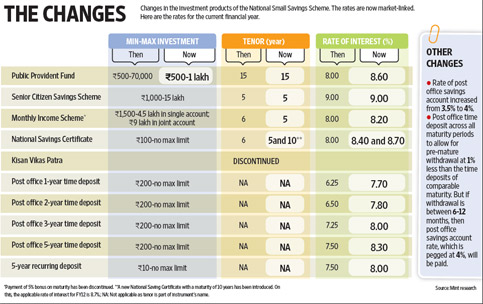

Given below are the changes in terms and interest rates for these savings schemes-

Source: Mint Money

Let’s have a look what they will mean to you once the changes are implemented:

PPF

One of the most lucrative saving schemes by the government has been made even more attractive. The ceiling of investment amount has been raised to Rs 1 lakh which is a welcome move for all investors. This amount will fall under section 80C and the tax benefit can be claimed. However, although the interest rate has been increase to 8.6%, what most investors are not aware of is that this rate is for FY 2011-2012 and not for 15 years. The interest rate has now been made market linked. It will now be benchmarked with Government Securities (G-Sec) of similar maturities and the interest rate will be 25 basis points above the G-Sec rate. So if a 10-year G-sec yields 8%, then the rate of interest for Public Provident Fund (PPF) would be 8.25%, 8% plus a mark up of 25 basis points. The government would declare the interest rate before 1 April every year.

What this means is that the maturity corpus will not be known unlike before. Since rates will vary every year the PPF maturity amount will very much rely on the assumption of interest rate government is going to declare.

Given below is the maturity amount of PPF in different interest rate scenarios-

Investment amount- Rs 1 lakh

Term of PPF- 15 years

Frequency | Interest Rate | Corpus (Rs lakh) | |

Scenario 1 | Through out | 8% | 29.32 |

Scenario 2 | First Year | 8.60% | |

Remaining Yrs | 8% | 29.34 | |

Scenario 3 | First Year | 8.6 | |

Remaining Yrs | 9% | 31.99 | |

Scenario 4 | First Year | 8.60% | |

Remaining Yrs | 7.50% | 28.1 |

As you can see the maturity amount varies with different interest rate. There can be other scenarios where interest rate might change more frequently.

Considering all these aspects it will be difficult for an investor to conclude the maturity amount beforehand. However what makes this instrument still an attractive proposition is the tax treatment. Even with varying interest rate the entire interest amount is tax free along with income tax benefit on the investment amount. Due to this the yield to the investors will still be much higher than other debt instruments.

One more positive change which will make investors stick to the basics of long term with PPF is the increase in interest rate on loans from 1% to 2%.

NSC

This instrument will now come with two different maturities – 5 year and 10 year. The interest rate decided for this year is 8.40% and 8.60%. However, unlike PPF the interest received here is taxable which will lower your post tax yield if interest rate declared by the government is too low.

Post Office MIS

The tenure of this savings instrument is being reduced to 5 years from 6 years. The interest rate declared this year is 8.20% and the bonus of 5% on maturity is being discontinued now. This option has been preferred by many retirees due to the fixed monthly interest it has offered. It can be a big setback for them as they no longer will be able to predict what monthly income this product will generate.

The increase in interest rate declared this year on PO Time deposit has been very high as compared to what was prevalent. For e.g. one year time deposit will now fetch you 7.70% instead of 6.25 % which is an increase of 1.45%.Similarly the other maturities of time deposit have also seen an increase of almost .50 to 1.30%. To provide high liquidity to investors, premature withdrawal is now allowed although with some penalty. This is a welcome move for investors’ looking for good alternatives during adverse market scenarios.

SCSS

There has been no change in this product this year except the interest rate being made market linked now. The tenure of the scheme remains the same which is good news for the senior citizens.

KVP

Kisan Vikas Patra has been discontinued now.

Although interest rate offered this year’s surely looks attractive what investors should be aware is that we are in high interest rate scenarios. Even the fixed deposits of banks are offering high rates now. As the interest rate start easing, the benchmark G-Sec yield will also start falling which will lower the interest rate on these savings schemes. What should worry investors is how much? And which is unpredictable.

With all these changes and the tax treatment offered to these instruments, PPF and SCSS still hold a good debt investment. One should continue investing in them for their long term goals.

Leave a Reply